Think of a Reserve DTF like the DRAM ETF, but on-chain, and let's suggest this AI DTF reaches $5 billion in six months. What happens next?

When the Vanguard asset management group started in 1975, it popularized the idea of mutual funds and, later on, ETFs - where a diversified portfolio of assets can be held together. They helped make it easy for an individual investor to buy in.

There is an argument that Vanguard founder John C. Bogle is one of the biggest philanthropists of all time, as he reduced the fees that were standard at the time to a minimum, saving investors $500 billion in fees in 50 years. And by forcing other providers to follow suit, small investors saved another $500 billion in fees.

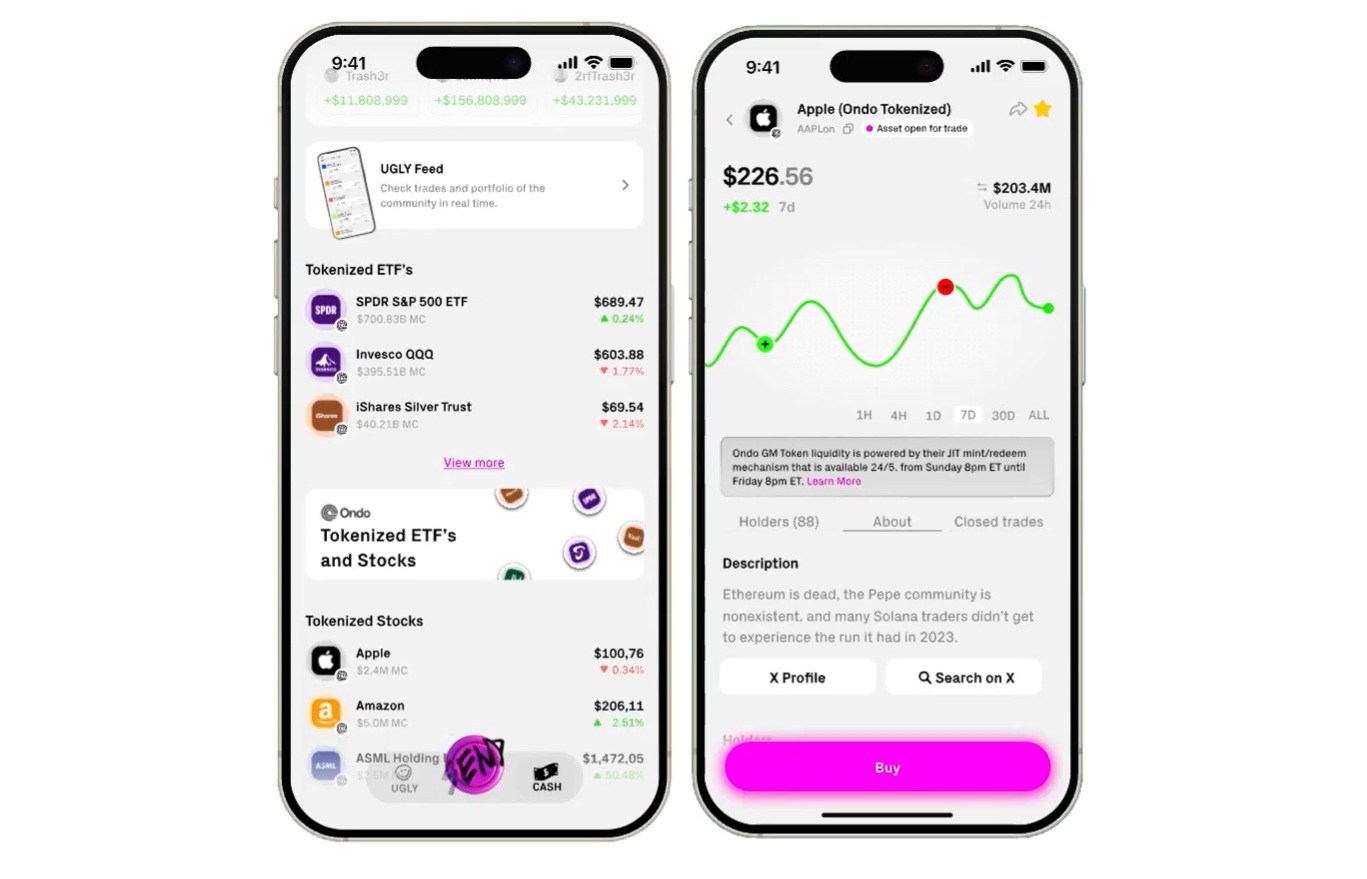

Why is this relevant? Let's take the recent Roundhill Memory ETF (DRAM), launched in April 2026, which offers a portfolio primarily of AI semiconductor/memory stocks (Samsung, Micron, Seagate, SanDisk) and has grown to $15.3 billion in assets under management. The demand is there, and everyday investors can choose to join in and set and forget.

Everyday investors... But $DRAM is a U.S.-listed ETF, limiting buyers to the U.S. and some countries or services that can access U.S. brokers. In effect, it is U.S.-only, unless you can jump a bunch of middleman hurdles.

So it's hard to access many ETFs - and not only access them, but access them without middlemen, without fuss, with none of the fees that come from all the brokerage that comes with ETFs.

Which is different with Reserve Protocol. Swap $100 USDT to Reserve's DTF, and you are in the market. We started with that Vanguard example of fee savings, because Reserve could abstract away even more fees, while making those portfolios available to people in ~145 countries who were previously cut off.

So let's play some hypotheticals, and place DTF success in the light of RSR holders.

What Happens to RSR if a Reserve Protocol DTF Hits $5 Billion TVL?

RSR's price is currently ~0.001c, with a supply of around ~65 billion. DTFs burn RSR according to their TVL management fee and minting fee.

For example, the CMC20 DTF has a market cap of $15 million and burns around 15 million RSR a month.

Think of a DTF like the DRAM ETF, but on-chain, and let's suggest this AI DTF reaches $1 billion in market cap after two months, and $5 billion in six months.

These figures may or may not be realistic - we shall see. The demand is likely there for global access to AI stocks, without the pain of seeking out individual shares to build your own portfolio. Buy one ERC-20 (or maybe BNB) token, and own a slice of 10 or 20 AI companies or however the DTF ends up looking.

So adjust your confidence zone accordingly, but based on this, how can we extrapolate how this might affect the burn and price of RSR over the next six months?

Let's build a rough model:

RSR price = ~$0.001

Supply = 65 billion

Market cap = $85 million

CMC20 market cap = $15 million

CMC20 burns ($) ≈ $15,000 a month

CMS20 burns (RSR at current price) ≈ 15 million RSR a month

Roughly 0.1% of the TVL per month per DTF flows into burning RSR.

An AI DTF reaching $5 billion TVL:

From $15 million to $5 billion is roughly 333× larger than CMC20.

Burn rate:

$15,000 x 333 = $5 million a month

At current price, a burn pressure of 15M RSR × 333 ≈ 5 billion RSR burned per month.

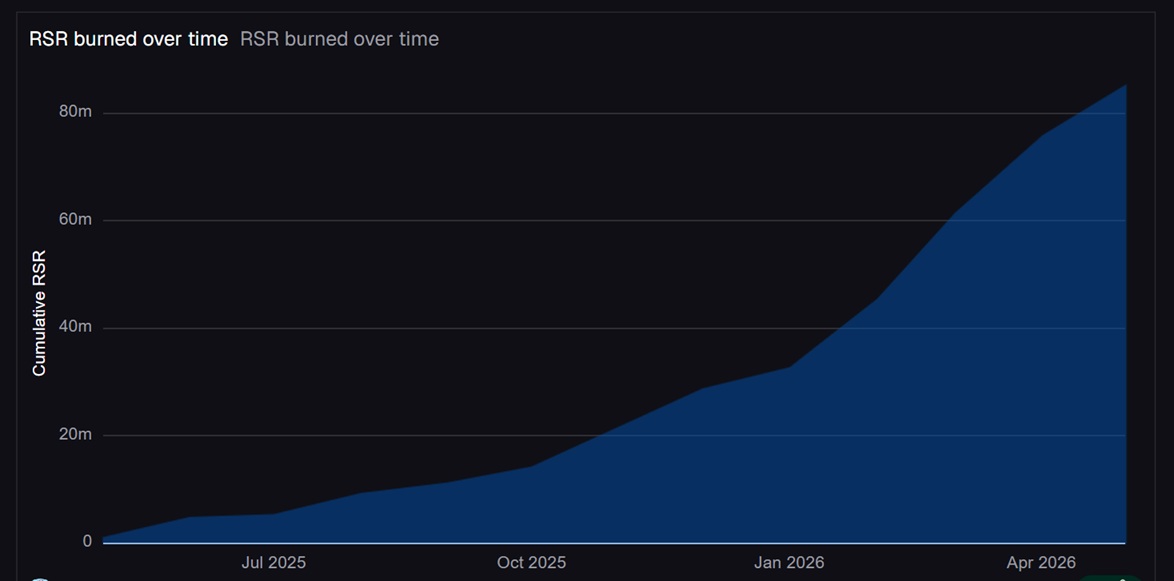

Six-month burn projection:

| Month | AI DTF TVL | RSR Burn |

| 2 | $1 billion | 1 billion |

| 3 | $2 billion | 2 billion |

| 4 | $3 billion | 3 billion |

| 5 | $4 billion | 4 billion |

| 6 | $5 billion | 5 billion |

| Total | $5 billion | 15 billion |

That could reduce the circulating supply of RSR to 50 billion, a 30% reduction in half a year.

The catch, of course, is that the burn will not stay linear because if the market keeps valuing RSR at $70 million (as it does today) while supply falls from 65B to 50B, the price rises automatically.

At unchanged market cap:

65B supply → $0.001

50B supply → $0.00133

That's already a 33% increase.

But that's the conservative scenario: a more realistic market reaction is that markets don't wait for burns to happen.

If traders see a $5B AI DTF, thanks to many investors in many countries accessing tokenized AI stock index portfolios, and up to 5B RSR a month disappearing, they start pricing future scarcity.

A simple RSR Valuation Approach Might Be:

What multiple of annual protocol revenue should RSR trade at?

Traditional ETF businesses often trade at 10-30x earnings.

If an AI DTF generated $50 million annually in RSR burns, the protocol valuation could move into the hundreds of millions or even billions.

That's where things get nonlinear, with a conservative scenario of the market cap rising from $65M to $200M.

A more aggressive scenario would be the RSR market cap reaches $1 billion with a circulating supply of 50 billion RSR (and 15 billion RSR burned forever), which would price RSR at about 2c per token - or a 20x from here.

The extreme scenario, one that RSR bulls dream about, is that AI DTFs become the default way for non-U.S. investors to access tokenized AI equities, and additional DTFs launch behind it. At that point, $5B TVL becomes the beginning, rather than the top.

If DTFs can find a $10-20B aggregate TVL, the market stops valuing RSR as a speculative governance token and starts valuing it as a claim on a rapidly growing on-chain asset-management business.

Even if the market completely ignored the DTF narrative and only reacted mechanically to shrinking supply, they would see the tokenomics become dramatically more deflationary than they are today. Based on the current CMC20 burn data and Reserve's fee-to-burn mechanism, the market would struggle to ignore deflationary supply of this magnitude.

One DTF is Good, But What About 10?

But the most interesting aspect can be that if one DTF becomes big, what comes next?

You can quickly reach an industry of:

- AI DTF

- Defence DTF

- Robotics DTF

- Biotech DTF

- Emerging markets DTF

- Dividend DTF

- Precious metals DTF

= The market starts valuing Reserve similarly to an on-chain version of BlackRock or State Street Global Advisors, rather than a crypto protocol.

At that point, Reserve stops competing with crypto projects and starts competing with traditional ETF infrastructure.

But what we want first is:

- 145 countries accessing U.S. stocks through DTFs

- 24/7 trading

- instant settlement

- composability with DeFi

- billions flowing on-chain

The key thing to watch isn't price:

It's whether that first AI DTF actually gets real demand from people who can't easily access U.S. markets. If that use case proves genuine, then the market eventually starts valuing Reserve as an asset management platform.

Next time you're bored, drop this into your favorite AI agent:

RSR's price is currently $0.001, with a supply of around 65 billion. DTFs burn RSR according to their TVL management fee and minting fee.

CMC20 has market cap of $15 million and burns around 15 million RSR a month.

A DTF launches next month, on on-chain index of tokenized AI stocks, available 24/7 to 145 countries which currently cannot access AI stocks in the US. Think of it like the DRAM ETF, but on-chain.

This DTF is expected to have 1 billion TVL in a month, and 5 billion TVL in six months.

Based on this, can you extrapolate how this might affect the burn and price of RSR over the next six months?