Best Crypto to Buy: RSR Looks Like The Next Big RWA Project

By Matthew

The "pilot phase" of 2023-2025 - where institutions like BlackRock and Franklin Templeton dipped their toes into on-chain treasuries - is over. We are now in the aggregation phase.

This is where Reserve Rights (RSR) enters.

For years, Reserve was misunderstood as just another stablecoin project. In early 2026, however, it is emerging as the primary infrastructure for indexing the chaotic sprawl of the RWA sector. As tokenized assets proliferate - from T-bills to private credit to commodities - investors will stop picking individual winners. They will buy the index.

Reserve is building the indices, and RSR is the asset that, depending on the the type of index, governs (or governs and insures) them.

The Aggregation Play

The RWA landscape today is a mess of fragmentation. You have BlackRock’s BUIDL, Ondo’s USDY, Superstate’s USTB, and dozens of other yield-bearing tokens scattered across different chains with different compliance whitelists. For a retail investor - or even a mid-sized DAO treasury - managing exposure to these individual assets is a headache.

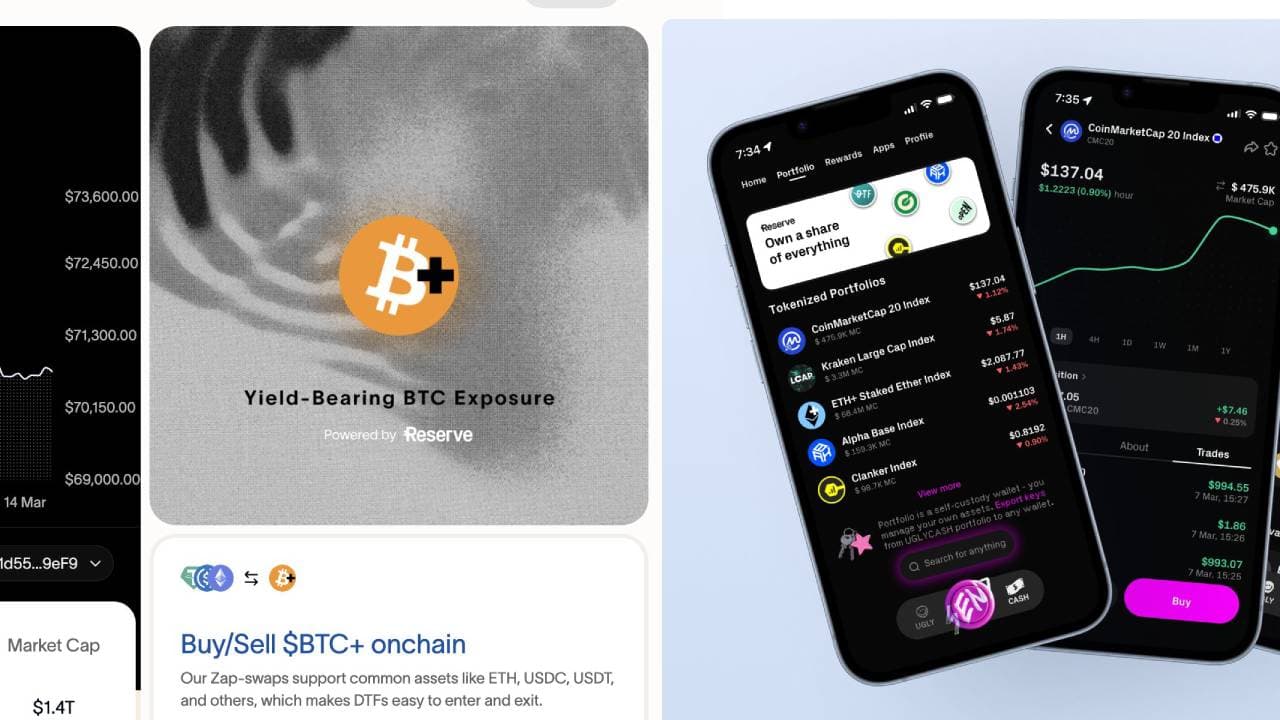

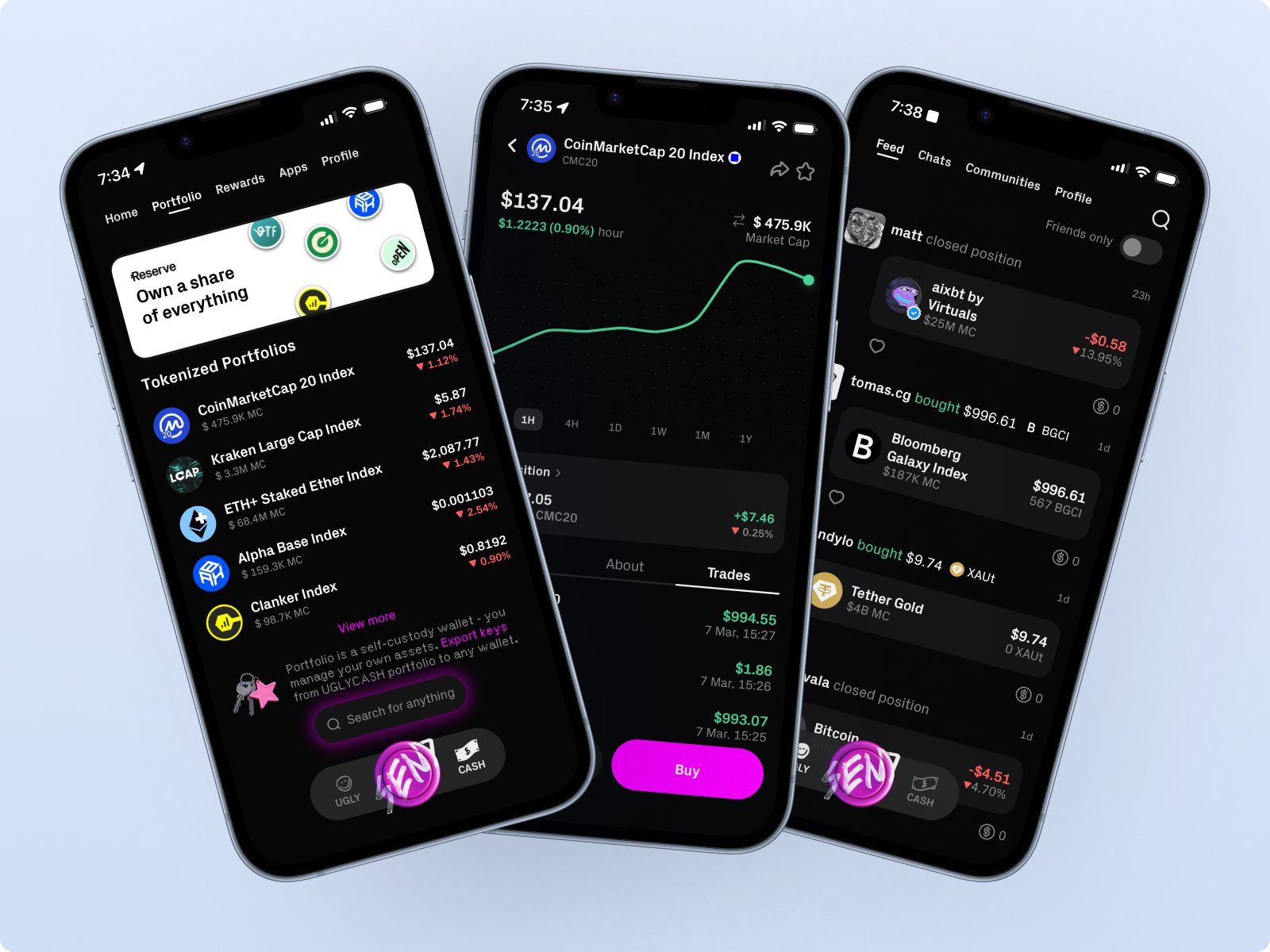

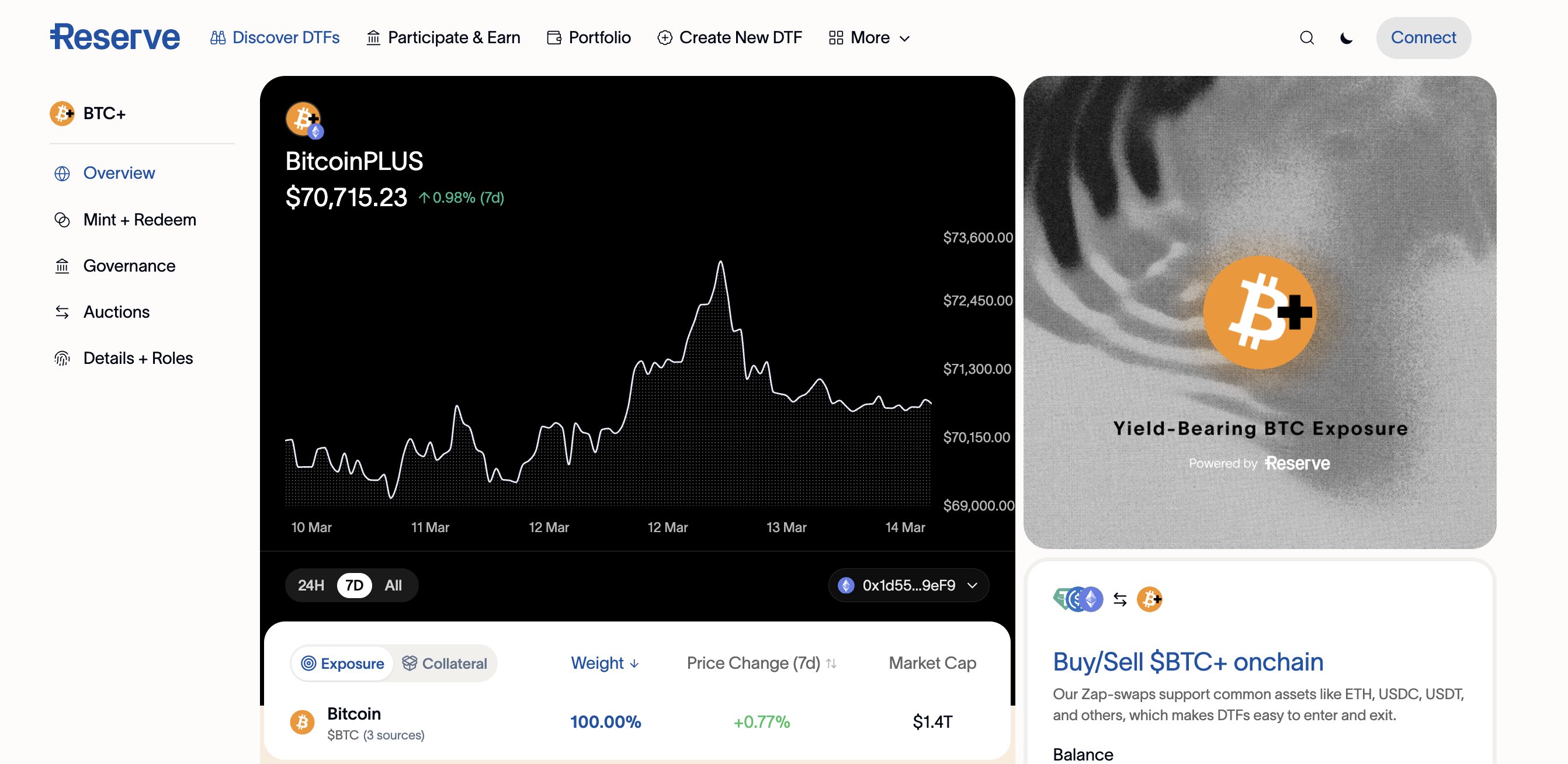

Reserve Protocol solves this by allowing anyone to deploy Decentralized Token Folios or DTFs. These are essentially on-chain ETFs. A DTF can be composed of anything on-chain - let’s for example, choose 33% BUIDL, 33% USDY, and 33% tokenized gold, wrapped into a single, permissionless ERC-20 token that automatically compounds yield.

You don't need to bet on whether BlackRock or Franklin Templeton wins the tokenized treasury war. You bet on the protocol that bundles them both into a product the market actually wants to use. Already, indexes such as CMC20 are finding their market.

The DTF Concept

A Decentralized Token Folio (DTF) is a basket of assets held in a smart contract. It allows users to get exposure to a theme (like "DeFi Blue Chips" or "Yield Bearing Stablecoins") by holding a single token.

Yield DTFs: These are typically stable-value baskets (like eUSD) or yield-bearing ETH baskets (like ETH+). They generate revenue from the underlying collateral. RSR holders stake on these to provide insurance.

Index DTFs: These are volatile baskets that track a market sector (e.g., a "Large Cap" DTF). They do not require insurance, but they generate fees that are used to buy and burn RSR.

The Governor Mechanism: Why RSR Has Value

Most governance tokens are relatively worthless. They offer "voting rights" on forums nobody reads. RSR is different because its governance is inextricably linked to financial liability.

RSR has two or three roles in the ecostem.

RSR serves as the governor token for “Index DTFs”, for a slice of the management fees

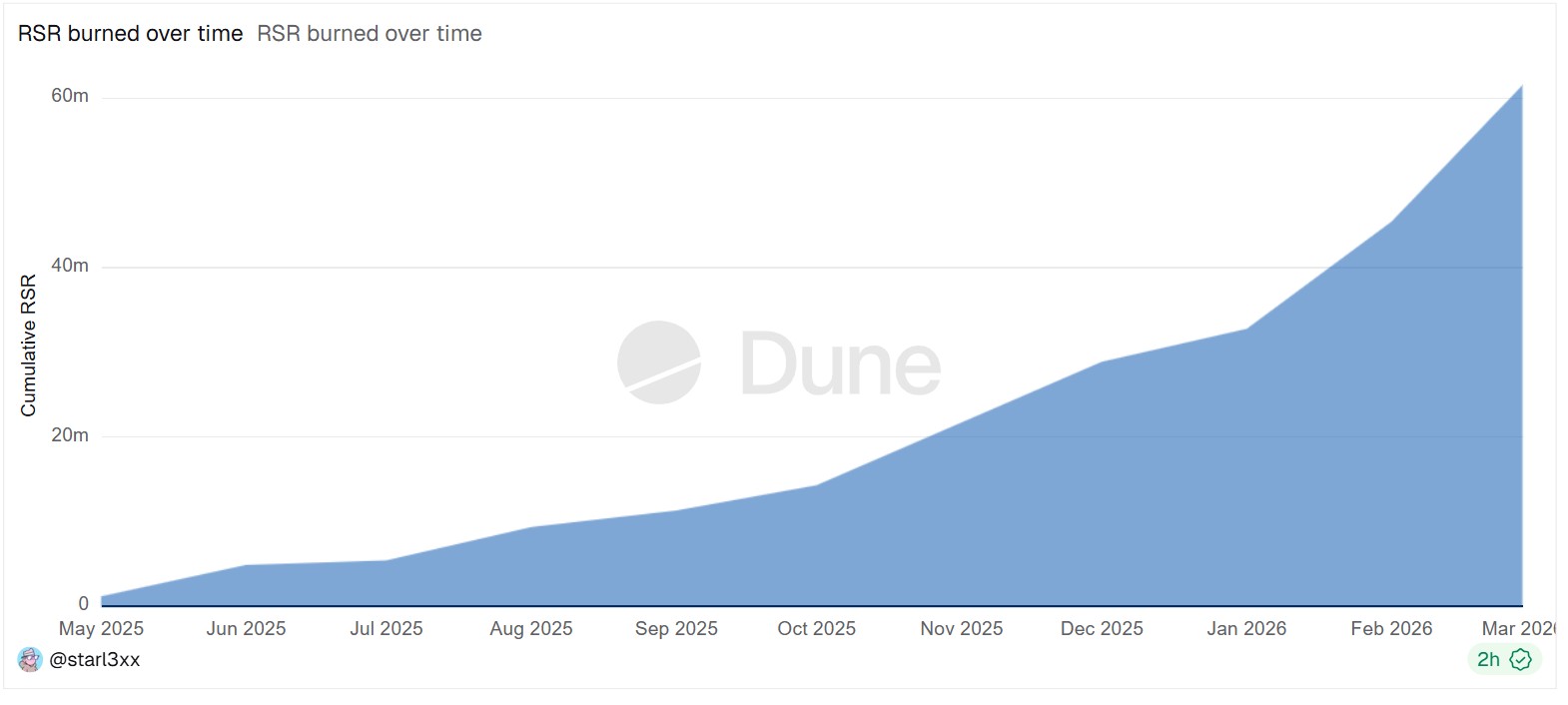

Management fees and minting fees also contribute to a monthly RSR burn, making the protocol deflationary

RSR serves as “first-loss governance” on “Yield DTFs”, or “RTokens”, where RSR governors also offer protection if the backing of a Yield DTF fails.

Let’s take the third one first. In the Reserve ecosystem, RSR holders stake their RSR on specific RTokens to insure them. This is the "protection" mechanism. If an underlying asset in the basket defaults - say, a specific private credit token depegs or a custodian freezes funds - the staked RSR is seized and auctioned off to make the RToken holders whole.

It is a brutal, direct mechanism. There is no bailout committee. The smart contracts, specifically the "Governor Anastasius" modules deployed across the ecosystem, execute this logic mercilessly.

But the upside is equally direct. In exchange for providing this first-loss capital, RSR stakers receive a portion of the revenue generated by the RToken, for instance eUSD, at the time of writing, offers 10% APY. As the market cap of RTokens grows, the yield flowing to RSR stakers increases.

In 2026, we are seeing RTokens offering yields that beat standard T-bills because they stack the underlying RWA yield with additional incentives. This attracts TVL (Total Value Locked). Higher TVL means more revenue for RSR stakers. More revenue drives demand for RSR. It is a reflexive loop that has not yet been fully priced in by the market.

DTFs and RTokens Begin to Capture the Market

The tokenized treasury market alone has crossed the multi-billion dollar mark. But the real explosion in 2026 is in "diversified cash" - stablecoins that aren't just dead money, but yield-bearing baskets.

If an RToken becomes the de facto "savings account" for on-chain users - offering the safety of diversified sovereign debt with the ease of a stablecoin - its market cap could rival USDC or USDT.

Currently, RSR trades at a valuation that implies it is a niche DeFi app. But if it functions as the insurance layer for a $10 billion or $50 billion RWA economy, the token mechanics force a repricing. The staking capacity (the amount of RSR available to insure RTokens) must grow to accommodate the TVL.

If the market demands $1 billion in insurance coverage for a popular RToken, and stakers demand a 10% APY for taking that risk, the protocol must generate $100 million in revenue. The market cap of RSR would likely expand to multiples of that insurance capacity.

The leverage here is on the adoption of the indices. Every dollar that moves from a raw stablecoin (like USDC) into a Reserve RToken (like a yield-bearing stable basket) is a direct catalyst for RSR value accrual.

Meanwhile, deployers are creating “index DTFs”, which forego the protection aspect but work as an on-chain tracker of on-chain assets: basically, an ETF, but without the hurdles, the paperwork, the middlemen or the downtime.

These can also offer yield to RSR stakers, and more importantly, the constant actions (minting, management fees) directly burn RSR, benefiting everyone in the ecosystem.

The market is currently mispricing RSR because it views it through the lens of the 2021 bull run - as just another DeFi governance token. It is failing to see the pivot to RWA infrastructure.

Reserve has spent the last two years building the pipes. The "Governor" contracts are live. The RTokens are minting. The underlying RWAs are finally liquid enough to be bundled.

We are looking at a protocol that allows the crypto market to abstract away the complexity of the real world. Investors don't want to do due diligence on 50 different tokenized bond issuances. They want a single token that yields 5% and doesn't go to zero.

Reserve builds that token. Well, technically, anyone can use the platform to build their own portfolio of RWA assets.

If the RWA narrative in 2026-20230 plays out as expected with trillions of dollars moving on-chain, then the RSR layer on that capital may become one of the most valuable assets in the ecosystem.

To explore current DTFs, visit https://app.reserve.org/.

Reserve News — Unofficial news about Reserve Protocol

Back to all articles

ble currencies) on Reserve.

ble currencies) on Reserve.