Reserve co-founder Nevin Freeman has outlined how the newly released version of the Uglycash app now features Reserve DTFs (on-chain indexes) prominently.

In a packed update, Reserve co-founder Nevin Freeman has outlined how the newly released version of the Uglycash app now features Reserve DTFs prominently, alongside tokenized equities and other crypto assets.

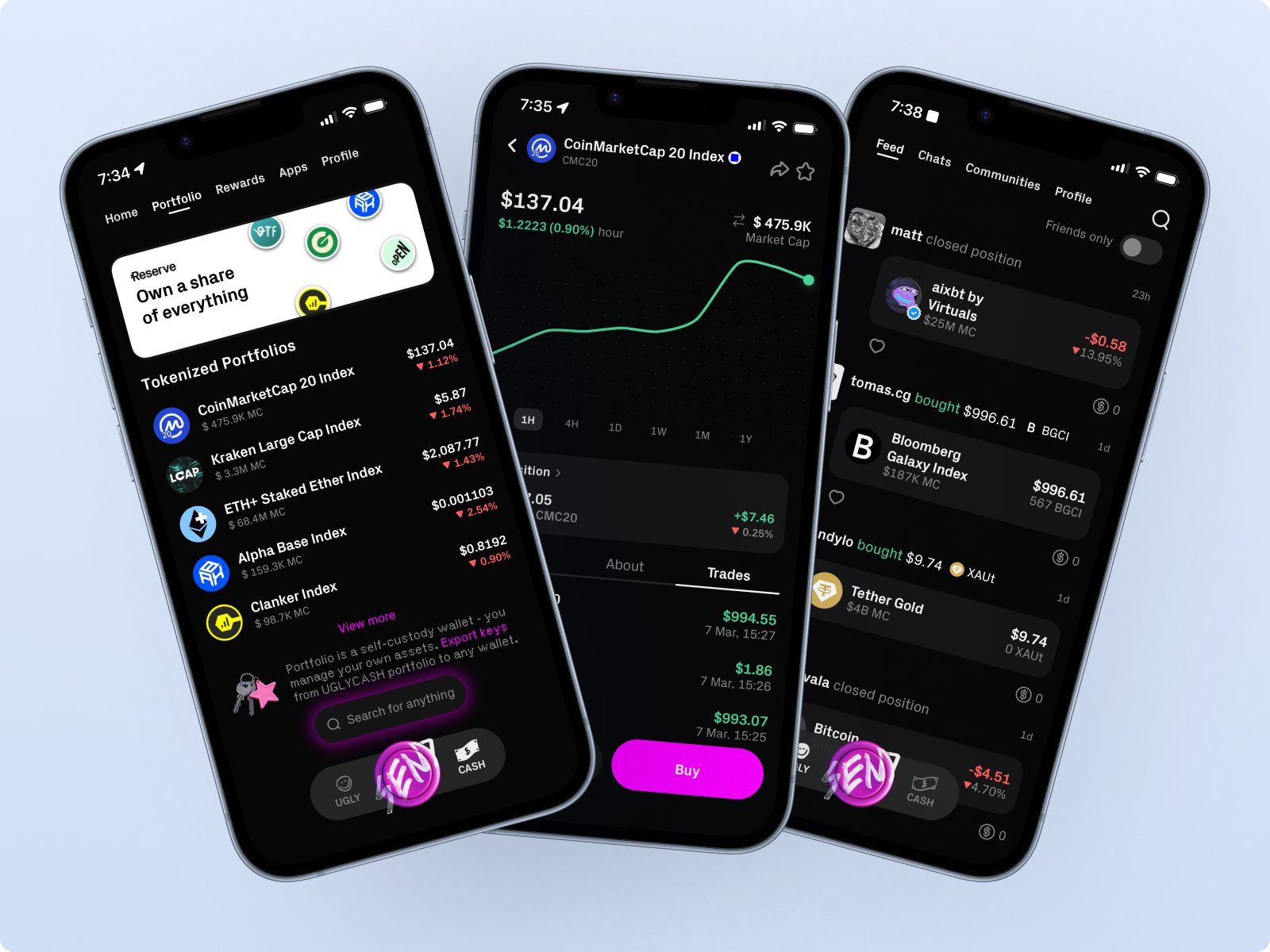

“UGLYCASH is our retail-facing app, designed to bring DTFs to a broader audience through a social trading experience rather than requiring users to interact with the protocol directly,” Freeman wrote.

Rather than searching through token lists or DeFi dashboards, users can discover assets through traders and communities they follow. Within the app, users can buy DTFs like CMC20, track portfolios, and interact with multiple chains from a single balance.

For users outside the United States, the experience goes further, as the new version also integrates tokenized stocks and ETFs through Ondo’s tokenized asset infrastructure, allowing equities to sit alongside crypto portfolios in the same interface. Availability varies by region, but it does make wallet a hybrid financial dashboard.

Early promotional campaigns inside the app include a trader leaderboard and social engagement rewards, intended to encourage discovery through the platform’s social layer rather than traditional asset search.

New DTF Experiments: BTC+, MCAP, and Harvest

Alongside the Uglycash revamp, the Reserve team introduced three new experimental DTFs to members of its “Top 100” testing group.

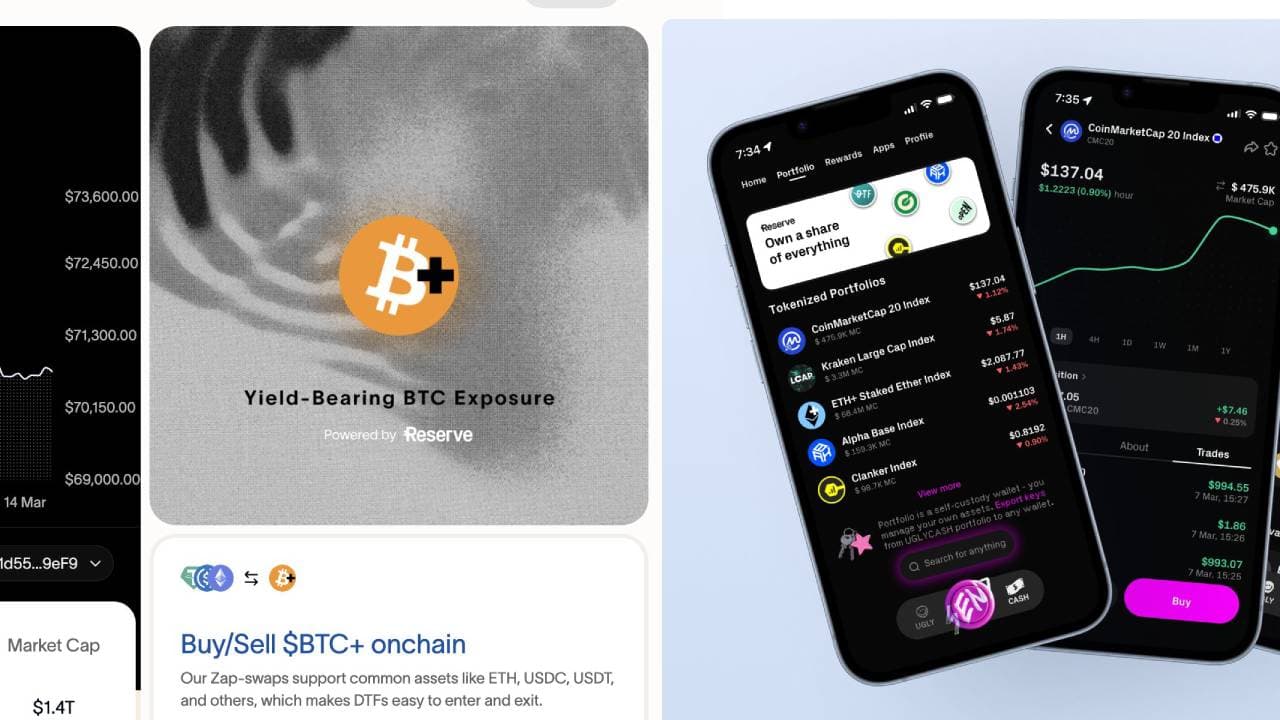

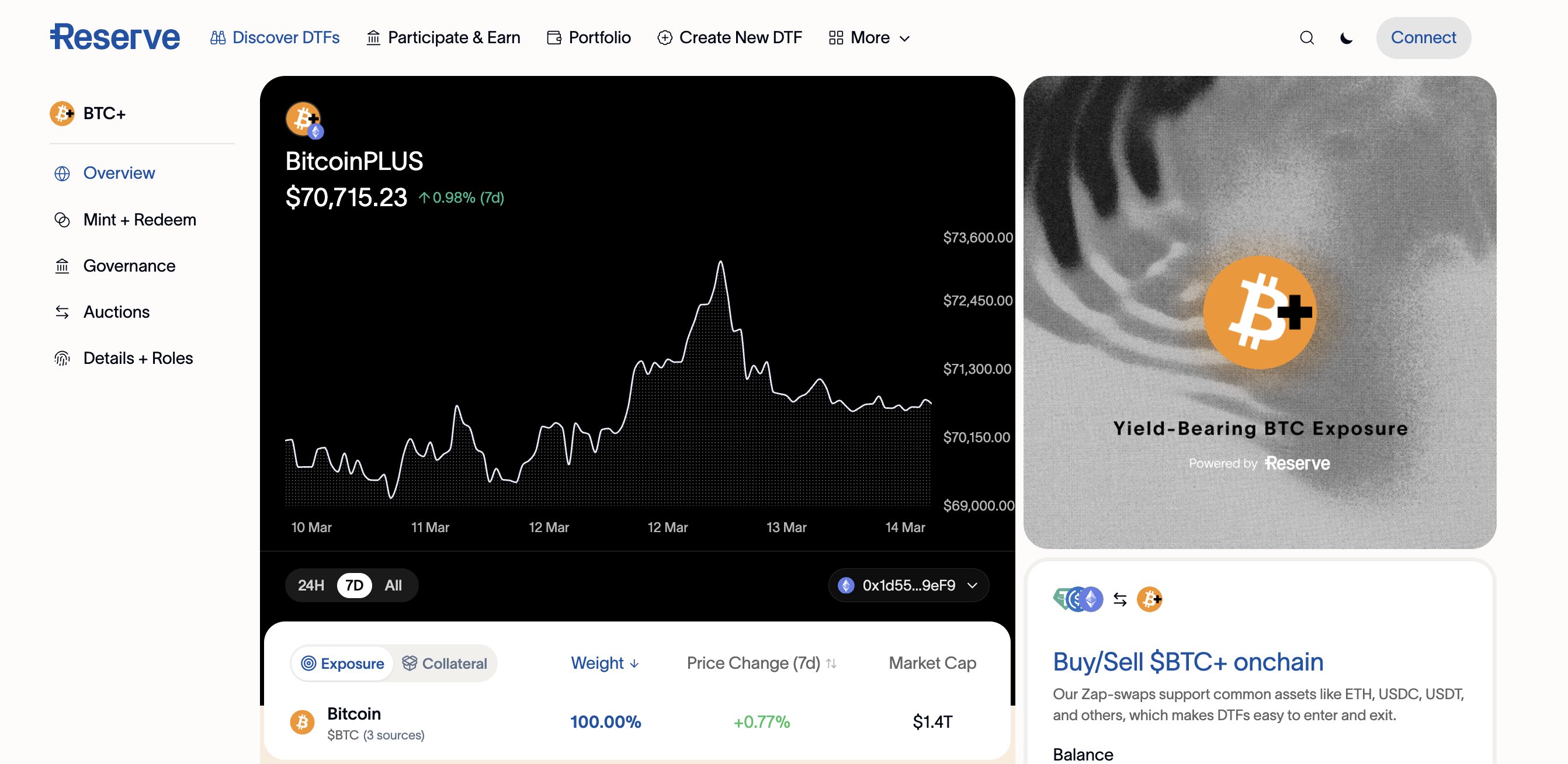

The most notable is BTC+, an index of yield-bearing Bitcoin positions packaged as a decentralized token folio. The basket currently includes liquidity pool positions across several Bitcoin wrappers, wBTC, cbBTC, and tBTC, with yield generated through trading fees.

Combined with a mechanism that redirects part of the mint fee to existing holders, the strategy is currently producing roughly 2.5% to 3.5% APY.

Two additional products were introduced during the same weekly sync.

MCAP packages Bitcoin and Ethereum exposure into a single token using a hybrid weighting approach, blending market capitalization and equal weighting.

Harvest, by contrast, is a volatility strategy with a portfolio that holds ETH and a yield-bearing stablecoin and rebalances whenever ETH moves by roughly ten percent, systematically buying dips and locking in gains.

Backtesting suggested the Harvest strategy could outperform pure ETH exposure while reducing volatility across multiple market regimes. For now, all three products remain limited to the Top 100 audience while the team observes real-world behavior.

eUSD Economics and Governance Evolution

Reserve’s stablecoin ecosystem is also undergoing changes. A community effort is underway to formalize the mandate and methodology for eUSD, the protocol’s dollar-denominated RToken used widely in fintech integrations. Governance delegate Ham is drafting a detailed framework covering basket composition, engineering requirements, and revenue mechanics.

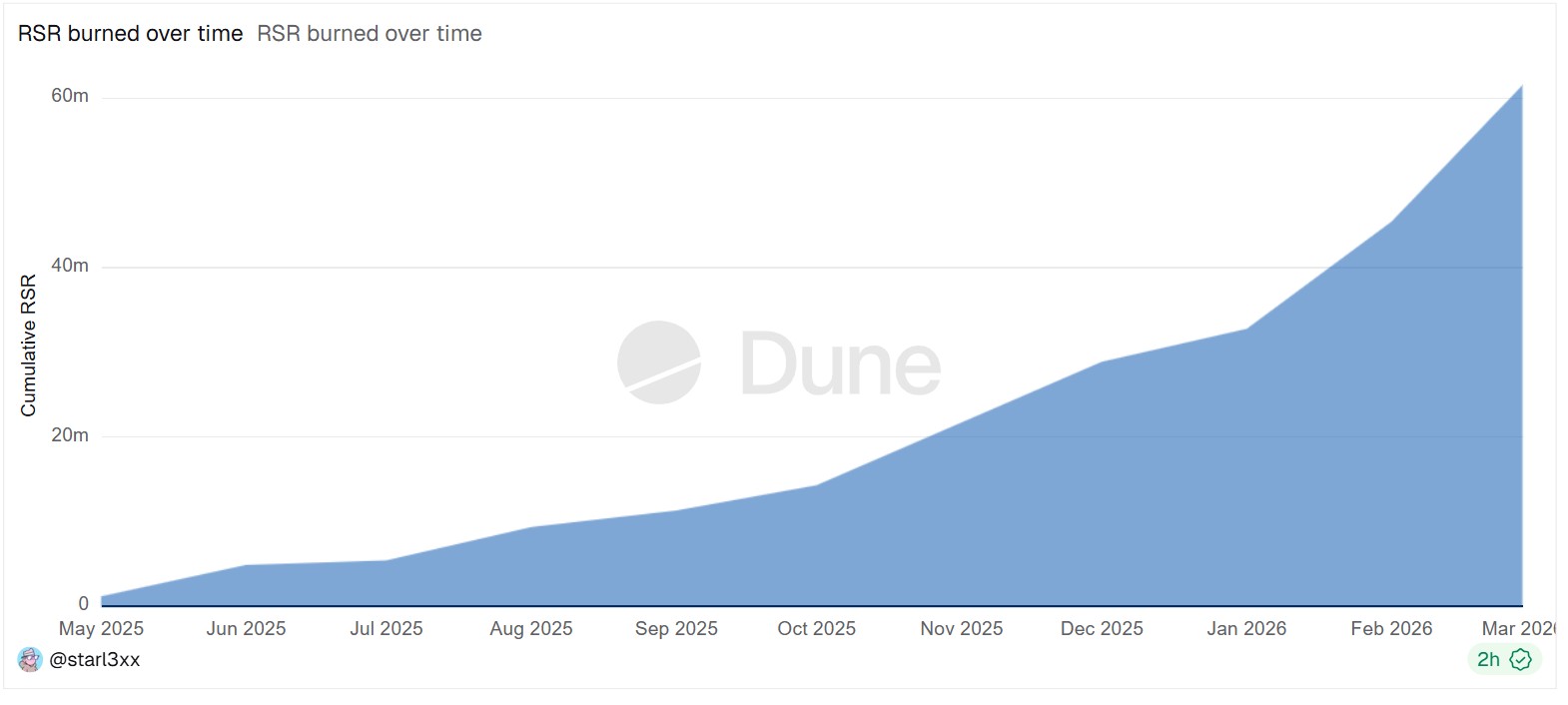

Part of that work involves clarifying how revenue flows through the ecosystem. Under the current structure, staked RSR receives 100% of revenue generated on eUSD balances held outside fintech wallets. In future, this may increase to include 10% of revenue generated on fintech-held balances.

The goal of the new documentation is to make those economics explicit and easier to understand for both developers and governance participants.

Freeman described the process as part of a broader effort to bring greater transparency and structure to how Reserve’s financial products evolve.

DSI and the Push Toward Tokenized Securities

Reserve’s Digital Securities Initiative (DSI) continues to explore how traditional securities might eventually move onchain.

The initiative, working alongside the Tokenized Asset Coalition, recently submitted a proposal to the U.S. Securities and Exchange Commission’s crypto task force outlining a framework known as the Global Access Protocol. The proposal argues for regulatory clarity that would allow tokenized securities to operate on blockchain infrastructure while still meeting compliance requirements.

Research work continues behind the scenes. According to Freeman, the DSI team has been studying multiple legal and technical models for securities tokenization, examining questions around transfer agents, shareholder registries, and proxy voting.

The effort remains exploratory, but the research is becoming increasingly detailed as the team prepares for eventual pilot programs.

Other Developments Across the Ecosystem

Freeman’s update also included a range of additional technical and product work underway across the Reserve ecosystem.

• The Reserve app portfolio page has been redesigned to show DTF holdings, staked RSR, governance proposals, and voting power in a single interface.

• An RFC proposes formally deprecating 17 dormant DTFs, allowing the ecosystem to focus attention on actively maintained products.

• The internal backtesting system gained a new Signals interface for designing custom weighting strategies.

• Research teams are experimenting with adaptive Bitcoin trading models such as Cycle-Aware moving averages and the Kaufman Adaptive Moving Average.

• Engineers are exploring how to integrate real-world assets with delayed settlement into DTF structures.

• The team is building purpose-built AI research tools after abandoning a generic agent framework that proved unsuitable for strategy development.

Freeman framed the work as part of a long-term effort to build the infrastructure for on-chain index products.

“Decentralized governance requires attention,” he wrote when discussing the deprecation of dormant DTFs. “We want to point people toward the products that are most likely to get sustained attention from their communities and curators.”

The full update runs much longer on the X thread, where the discussion continues.

ble currencies) on Reserve.

ble currencies) on Reserve.